Breaking Down Canada’s 2026 Federal Tax Brackets

The Canada Revenue Agency (CRA) has officially announced the federal income tax brackets for 2026, featuring a landmark change: the first full year of the reduced 14% tax rate on the lowest bracket. Combined with a 2.0% indexation adjustment and an increased Basic Personal Amount (BPA), these changes will impact millions of Canadian taxpayers.

Whether you’re planning salary negotiations, maximizing RRSP contributions, or simply preparing for next year’s tax season, understanding these updates is essential for effective financial planning.

2026 Federal Income Tax Brackets at a Glance

Canada’s progressive tax system divides your income into segments, taxing each portion at its corresponding rate. Here are the official 2026 federal tax brackets:

Breaking Down Canada’s 2026 Federal Tax Brackets

The Canada Revenue Agency (CRA) has officially announced the federal income tax brackets for 2026, featuring a landmark change: the first full year of the reduced 14% tax rate on the lowest bracket. Combined with a 2.0% indexation adjustment and an increased Basic Personal Amount (BPA), these changes will impact millions of Canadian taxpayers.

Whether you’re planning salary negotiations, maximizing RRSP contributions, or simply preparing for next year’s tax season, understanding these updates is essential for effective financial planning.

2026 Federal Income Tax Brackets at a Glance

Canada’s progressive tax system divides your income into segments, taxing each portion at its corresponding rate. Here are the official 2026 federal tax brackets:

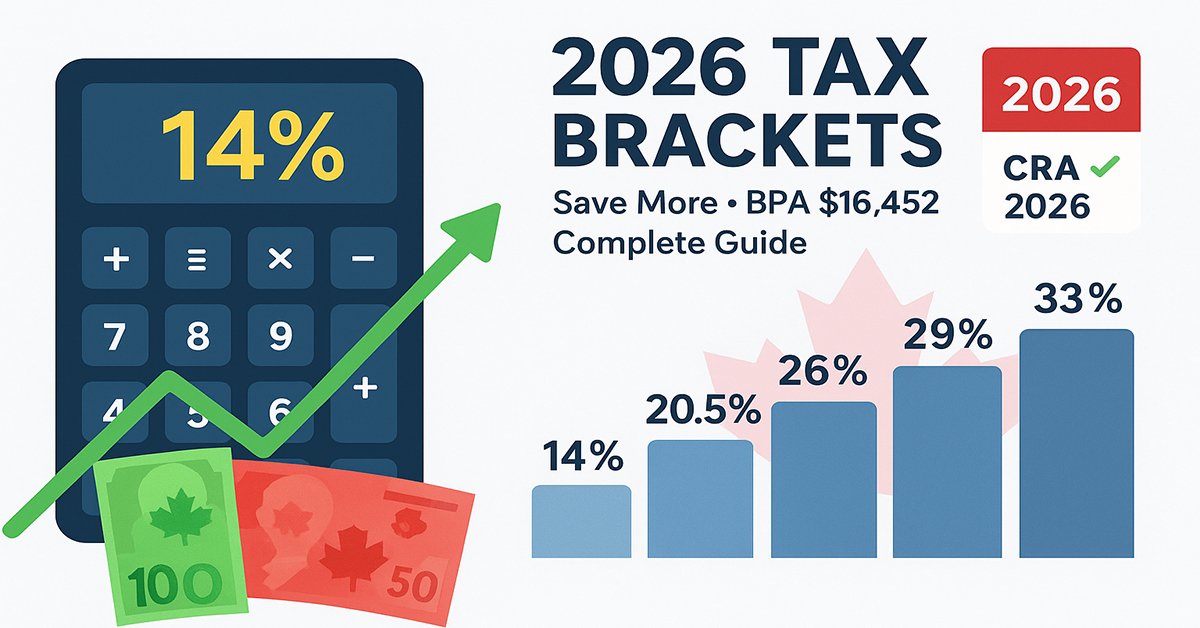

| Tax Rate | Income Range |

| $14\%$ | $\$0$ to $\$58,523$ |

| $20.5\%$ | $\$58,524$ to $\$117,045$ |

| $26\%$ | $\$117,046$ to $\$181,440$ |

| $29\%$ | $\$181,441$ to $\$258,482$ |

| $33\%$ | Over $\$258,482$ |

What’s New for 2026

Full-Year 14% Rate: This marks the first complete tax year with the reduced lowest bracket rate. In 2025, the rate was effectively 14.5% due to the mid-year implementation on July 1.

2.0% Indexation: All bracket thresholds have increased by 2.0%, protecting taxpayers from bracket creep caused by inflation.

Higher BPA: The Basic Personal Amount has increased to $16,452 for most Canadians, meaning more income is tax-free.

Understanding the 14% Federal Tax Rate

How the Rate Reduction Works

The federal government permanently reduced the lowest tax bracket from 15% to 14% for 2025 and beyond. Here’s what this means for 2026:

Universal Benefit: Every Canadian taxpayer saves on the first $58,523 of taxable income, regardless of total earnings.

Full-Year Impact: Unlike 2025’s partial-year application, the 14% rate applies to all twelve months of 2026, maximizing savings.

Amplified by BPA: When combined with the Basic Personal Amount, lower- and middle-income earners see the most significant percentage savings.

Real Dollar Savings

Compared to the previous 15% rate, a Canadian earning $58,523 saves approximately $585 annually just from this rate reduction alone—before factoring in the increased BPA and indexation benefits.

The 2026 Basic Personal Amount Explained

The Basic Personal Amount (BPA) is Canada’s most important non-refundable tax credit. It represents the income threshold below which you pay zero federal tax.

2026 BPA Breakdown

- Maximum BPA: $16,452 (for incomes up to $181,440)

- Minimum BPA: $14,829 (for incomes of $258,482 and above)

- Phase-out Range: BPA gradually reduces for incomes between these thresholds

Who Benefits Most

Income Below $16,452: You owe zero federal income tax Income Between $16,452 and $181,440: You receive the full BPA credit Income Between $181,440 and $258,482: Your BPA gradually reduces Income Above $258,482: You receive the minimum BPA of $14,829

The income-tested structure ensures tax relief targets those who need it most while still providing benefits to all income levels.

Complete Tax Calculation Example: $140,000 Income

Let’s walk through a detailed calculation for someone earning $140,000 in taxable income for 2026:

Step-by-Step Breakdown

Step 1: Apply the Basic Personal Amount

- First $16,452: $0 tax (covered by BPA)

Step 2: Calculate Tax on Each Bracket

- Next $42,071 (14% bracket): $5,889.94

- Next $58,522 (20.5% bracket): $11,997.01

- Remaining $22,955 (26% bracket): $5,968.30

Total Federal Tax Owed: $23,855.25

Effective Federal Tax Rate: 17.04%

Note: This excludes provincial taxes, additional credits (like pension contributions, childcare, medical expenses), and deductions (RRSP, union dues, etc.).

2026 vs 2025: Side-by-Side Comparison

Understanding what changed helps you identify where savings will appear.

2025 Federal Tax Brackets

- 14.5% on the first $57,375

- 20.5% on $57,376 to $114,750

- 26% on $114,751 to $177,882

- 29% on $177,883 to $253,414

- 33% above $253,414

2025 Basic Personal Amount

- $16,129 for incomes below $177,882

- $14,538 for incomes above $253,414

Key Changes in 2026

✓ Lower rate (14% vs 14.5%) for full year ✓ Higher bracket thresholds across all levels ✓ Increased BPA ($16,452 vs $16,129) ✓ 2.0% indexation adjustment ✓ Expanded income ranges before hitting higher rates

Federal Tax Liability Table for 2026

Based on 2026 tax brackets and BPA of $16,452 (assumes no other credits or deductions):

| Taxable Income | Federal Tax Owed | Effective Rate |

| $\$20,000$ | $\$503$ | $2.51\%$ |

| $\$30,000$ | $\$1,903$ | $6.34\%$ |

| $\$40,000$ | $\$3,303$ | $8.25\%$ |

| $\$50,000$ | $\$4,703$ | $9.40\%$ |

| $\$58,523$ | $\$5,890$ | $10.06\%$ |

| $\$70,000$ | $\$7,281$ | $10.40\%$ |

| $\$80,000$ | $\$9,386$ | $11.73\%$ |

| $\$90,000$ | $\$11,491$ | $12.77\%$ |

| $\$100,000$ | $\$13,596$ | $13.59\%$ |

| $\$117,045$ | $\$17,001$ | $14.53\%$ |

| $\$125,000$ | $\$19,081$ | $15.26\%$ |

| $\$140,000$ | $\$23,855$ | $17.04\%$ |

| $\$160,000$ | $\$29,025$ | $18.14\%$ |

| $\$181,440$ | $\$35,185$ | $19.40\%$ |

| $\$200,000$ | $\$40,705$ | $20.35\%$ |

| $\$225,000$ | $\$48,955$ | $21.76\%$ |

| $\$250,000$ | $\$57,205$ | $22.88\%$ |

| $\$258,482$ | $\$59,652$ | $23.08\%$ |

| $\$300,000$ | $\$72,452$ | $24.15\%$ |

| $\$400,000$ | $\$105,452$ | $26.36\%$ |

How to Read This Table

- Taxable Income: Your income after all deductions

- Federal Tax Owed: Tax calculated using progressive brackets

- Effective Rate: Actual percentage of total income paid in federal tax

Notice how the effective rate remains significantly lower than the marginal rate for most income levels—this is the benefit of progressive taxation.

Understanding Tax Indexation: Your Inflation Protection

Indexation is the automatic adjustment of tax brackets and credits to account for inflation. Without it, taxpayers would experience “bracket creep”—being pushed into higher tax brackets without any increase in purchasing power.

How 2.0% Indexation Helps You

Higher Thresholds: You can earn more before entering higher tax brackets Increased Credits: The BPA and other credits rise with inflation Stable Real Tax Burden: Your effective tax rate doesn’t increase solely due to inflation Automatic Protection: No action required—CRA applies indexation automatically

Why 2.0% Matters

The 2026 indexation rate of 2.0% is lower than 2025’s 2.7%, reflecting Canada’s moderating inflation rate. While smaller than previous years, this adjustment still provides meaningful protection for all taxpayers.

Strategic Tax Planning for 2026

Understanding your position within the tax bracket structure opens opportunities for significant savings.

1. Maximize RRSP Contributions

Registered Retirement Savings Plan contributions reduce your taxable income, potentially moving you into a lower bracket.

Strategic Contribution Points:

- Reduce income below $117,045 to avoid the 26% bracket

- Reduce income below $181,440 to avoid the 29% bracket

- Reduce income below $258,482 to maximize BPA benefits

Example Benefit: A taxpayer earning $120,000 who contributes $3,000 to their RRSP drops from the 26% bracket to the 20.5% bracket on that income, saving $165 in federal tax alone (plus provincial savings).

2026 RRSP Contribution Limit: 18% of 2025 earned income, up to $32,490

2. Optimize TFSA Strategy

While Tax-Free Savings Accounts don’t reduce taxable income, they offer tax-free investment growth.

2026 TFSA Contribution Limit: $7,000 (unchanged from 2024-2025)

Best Uses for High-Income Earners:

- Tax-free capital gains (avoiding additional income in higher brackets)

- Emergency fund growth without tax implications

- Supplement to RRSP for retirement planning

3. Leverage Charitable Donations

Donation tax credits reduce your final tax bill and become increasingly valuable at higher incomes.

Federal Credit Rates:

- 15% on the first $200 donated

- 29% on amounts over $200 (33% for highest earners)

Strategic Timing: Group donations across years to exceed the $200 threshold more frequently, maximizing the higher credit rate.

- → New Canada Benefit Payments Arriving This Week in May 2026

- → Canada Bread Settlement Payments Begin Rolling Out Across Canada in 2026

- → Canada Immigration Backlog Update 2026: IRCC Application Inventory Crosses 2.15 Million

- → Canada Expands Visa-Free Travel Access for Citizens of Indonesia and Malaysia in 2026

- → Canada’s 365-Day Maintained Status Work Rule in 2026: What Foreign Workers Need to Know

- → Canada Launches Early Retirement Incentive Program in 2026: Eligibility, Benefits, and Application Process Explained

- → Bringing Your Family to New Zealand on a Work Visa: Complete 2026 Guide

4. Time Income and Bonuses Strategically

If you have control over when you receive income:

Consider Deferring Income If:

- You’re near a bracket threshold

- You expect lower income next year

- You want to preserve the full BPA

Consider Accelerating Income If:

- You’re in a temporarily low-income year

- You expect significantly higher income next year

- You’ve maximized current-year deductions

5. Claim All Eligible Credits and Deductions

Beyond the BPA, numerous credits can reduce your tax burden:

- Canada Employment Amount: $1,433 for 2026

- Public Transit Amount: For eligible transit passes

- Home Office Expenses: If working from home

- Medical Expenses: Amounts exceeding 3% of income

- Tuition and Education Credits: For students or carried forward

- Disability Tax Credit: $9,872 for 2026

- Caregiver Credits: For supporting dependents

Impact Analysis by Income Level

Low-Income Canadians (Under $40,000)

Primary Benefits:

- Full BPA application means minimal or no federal tax

- 14% rate maximizes take-home pay on earned income

- Enhanced benefits from refundable credits (GST/HST, CCB)

Example Impact: A single person earning $30,000 pays just $1,903 in federal tax—an effective rate of 6.34%. The 14% rate and increased BPA save approximately $350 annually compared to the old 15% system.

Middle-Income Canadians ($40,000-$120,000)

This group represents the majority of Canadian workers, including teachers, nurses, trades professionals, administrative staff, and early-career professionals.

Primary Benefits:

- Longest duration in lower tax brackets due to indexation

- Full BPA application (for incomes below $181,440)

- Maximum percentage savings from rate reduction

- RRSP contributions highly effective

Example Impact: A middle-income earner at $80,000 pays $9,386 in federal tax (11.73% effective rate). The combined benefit of the 14% rate, indexation, and higher BPA saves approximately $600-800 annually.

High-Income Canadians (Over $180,000)

High earners still benefit from changes, though the percentage impact is smaller.

Primary Benefits:

- Lower rates apply to first $181,440 of income

- Indexation delays entry into 29% and 33% brackets

- Strategic RRSP contributions most valuable

- Partial BPA still available

Planning Priorities:

- Maximize RRSP room ($32,490 limit for 2026)

- Consider income splitting with spouse

- Leverage charitable donations at 29-33% credit rate

- Explore business structure optimization if self-employed

Example Impact: An earner at $300,000 pays $72,452 in federal tax (24.15% effective rate). While the dollar savings from rate changes are larger, the percentage benefit is smaller than for middle-income earners.

Federal vs Provincial Tax Considerations

Federal brackets represent only part of your total tax burden. Each province and territory maintains separate tax systems.

Provincial Tax Structure Overview

Multi-Bracket Systems: Most provinces use progressive brackets similar to federal (Ontario, BC, Manitoba, Nova Scotia, etc.)

Single-Rate Systems: Alberta uses a flat 10% provincial tax on all taxable income

Separate Collection: Quebec administers its own tax collection independent of CRA

Variable Rates: Provincial rates range from 10% (Alberta) to over 20% (highest Quebec bracket)

Combined Federal-Provincial Examples

Alberta (Flat 10%):

- $80,000 income: ~$9,386 federal + ~$6,355 provincial = $15,741 total

Ontario (Progressive):

- $80,000 income: ~$9,386 federal + ~$3,770 provincial = $13,156 total

British Columbia (Progressive):

- $80,000 income: ~$9,386 federal + ~$4,480 provincial = $13,866 total

Quebec (Separate System):

- Unique calculations with different brackets and credits

Planning Implications

Always calculate both federal and provincial taxes together. Strategies that optimize federal taxes may have different impacts provincially.

Example: RRSP contributions save at your marginal rate for both systems. A $5,000 RRSP contribution in the 26% federal bracket + 12% provincial bracket saves $1,900 total.

Common Questions About 2026 Tax Brackets

How do I know which tax bracket I’m in?

Your tax bracket is determined by your taxable income—not your gross salary. Taxable income is calculated after all deductions (RRSP, union dues, childcare, etc.) are subtracted from your total income.

Does my entire income get taxed at my highest rate?

No. Canada uses a progressive system where only the income within each bracket is taxed at that bracket’s rate. Lower portions of your income are always taxed at lower rates.

When should I make RRSP contributions for 2026?

You can make RRSP contributions for the 2026 tax year from January 1, 2026, through March 2, 2027 (the RRSP deadline for the 2026 tax year).

How do federal changes affect my provincial taxes?

Federal bracket changes don’t directly change provincial brackets, but your taxable income (after federal deductions) flows to your provincial return, so strategies that reduce federal taxes often reduce provincial taxes too.

Will I get a refund in 2027 when filing my 2026 taxes?

Refunds depend on whether your employer withheld more tax than you owe. The lower 14% rate may result in slightly smaller refunds if payroll adjustments account for the change, but your total tax paid will be lower.

Key Takeaways for Canadian Taxpayers

What You Need to Remember

✓ 14% Rate is Permanent: The reduced lowest bracket rate applies to all Canadians for the entire 2026 tax year

✓ Higher BPA Means More Tax-Free Income: $16,452 of income is federally tax-free for most Canadians

✓ Indexation Provides Automatic Protection: 2.0% adjustment prevents inflation-driven tax increases

✓ Plan Around Thresholds: Understanding bracket boundaries helps optimize RRSP contributions and income timing

✓ Provincial Taxes Matter: Always consider your total tax picture, not just federal

✓ Early Planning Pays Off: Understanding 2026 brackets now allows for year-long tax optimization

Action Steps for 2026

- Calculate Your Expected Taxable Income: Include salary, investment income, and other sources

- Identify Your Marginal Tax Bracket: Determine which rate applies to your last dollar of income

- Review RRSP Contribution Room: Check your 2025 Notice of Assessment for available contribution space

- Plan Strategic Contributions: Time RRSP and TFSA contributions for maximum benefit

- Track Deductible Expenses: Keep records of medical expenses, charitable donations, and work-related costs

- Adjust Payroll Withholding if Needed: Speak with your employer if you anticipate significant tax changes

- Consider Professional Advice: Complex situations benefit from accountant or tax planner consultation

Frequently Asked Questions

What are the 2026 federal tax brackets in Canada?

The 2026 federal tax brackets are:

- 14% on income up to $58,523

- 20.5% on income from $58,524 to $117,045

- 26% on income from $117,046 to $181,440

- 29% on income from $181,441 to $258,482

- 33% on income over $258,482

These rates apply only to federal taxes; provincial taxes are additional.

What is the Basic Personal Amount for 2026?

The Basic Personal Amount (BPA) for 2026 is $16,452 for individuals earning $181,440 or less. It phases down to $14,829 for those earning $258,482 or more. If you earn less than $16,452, you pay no federal income tax.

How much federal tax will I pay on $100,000 in 2026?

On $100,000 of taxable income in 2026, you’ll pay approximately $13,596 in federal tax (13.59% effective rate) after applying the Basic Personal Amount. This doesn’t include provincial taxes or additional credits and deductions you may qualify for.

What’s the difference between the 2025 and 2026 tax brackets?

The 2026 brackets feature a full-year 14% lowest rate (compared to 14.5% effective rate in 2025), higher income thresholds due to 2.0% indexation, and an increased Basic Personal Amount of $16,452 (up from $16,129 in 2025).

How does the 14% tax rate save me money?

The 14% rate on the first $58,523 of taxable income saves you approximately 1% on that income compared to the previous 15% rate. For someone earning $60,000, this represents roughly $585 in savings annually, plus additional savings from the increased BPA.

Do the 2026 federal tax brackets include provincial taxes?

No. The federal brackets cover only federal income tax. Each province and territory has separate tax brackets and rates that apply in addition to federal taxes. Your total tax burden is the combination of both systems.

Final Thoughts: Making 2026 Work for You

The 2026 federal tax changes—while modest compared to some previous years—deliver meaningful relief to Canadian taxpayers across all income levels. The combination of the full-year 14% rate, 2.0% indexation, and increased Basic Personal Amount creates opportunities for smart financial planning.

Whether you’re a young professional just starting your career, a middle-income family managing household expenses, or a high earner optimizing tax efficiency, understanding these brackets helps you keep more of your hard-earned income.

Start planning now to maximize your 2026 tax position. Review your income projections, calculate your estimated tax liability, optimize your RRSP and TFSA contributions, and consider consulting with a tax professional for personalized strategies.

Remember: Tax planning is a year-round activity, not just a spring scramble. The earlier you start, the more options you have to reduce your tax burden legally and effectively.

| Tax Rate | Income Range |

| $14\%$ | $\$0$ to $\$58,523$ |

| $20.5\%$ | $\$58,524$ to $\$117,045$ |

| $26\%$ | $\$117,046$ to $\$181,440$ |

| $29\%$ | $\$181,441$ to $\$258,482$ |

| $33\%$ | Over $\$258,482$ |

What’s New for 2026

Full-Year 14% Rate: This marks the first complete tax year with the reduced lowest bracket rate. In 2025, the rate was effectively 14.5% due to the mid-year implementation on July 1.

2.0% Indexation: All bracket thresholds have increased by 2.0%, protecting taxpayers from bracket creep caused by inflation.

Higher BPA: The Basic Personal Amount has increased to $16,452 for most Canadians, meaning more income is tax-free.

Understanding the 14% Federal Tax Rate

How the Rate Reduction Works

The federal government permanently reduced the lowest tax bracket from 15% to 14% for 2025 and beyond. Here’s what this means for 2026:

Universal Benefit: Every Canadian taxpayer saves on the first $58,523 of taxable income, regardless of total earnings.

Full-Year Impact: Unlike 2025’s partial-year application, the 14% rate applies to all twelve months of 2026, maximizing savings.

Amplified by BPA: When combined with the Basic Personal Amount, lower- and middle-income earners see the most significant percentage savings.

Real Dollar Savings

Compared to the previous 15% rate, a Canadian earning $58,523 saves approximately $585 annually just from this rate reduction alone—before factoring in the increased BPA and indexation benefits.

The 2026 Basic Personal Amount Explained

The Basic Personal Amount (BPA) is Canada’s most important non-refundable tax credit. It represents the income threshold below which you pay zero federal tax.

2026 BPA Breakdown

- Maximum BPA: $16,452 (for incomes up to $181,440)

- Minimum BPA: $14,829 (for incomes of $258,482 and above)

- Phase-out Range: BPA gradually reduces for incomes between these thresholds

Who Benefits Most

Income Below $16,452: You owe zero federal income tax Income Between $16,452 and $181,440: You receive the full BPA credit Income Between $181,440 and $258,482: Your BPA gradually reduces Income Above $258,482: You receive the minimum BPA of $14,829

The income-tested structure ensures tax relief targets those who need it most while still providing benefits to all income levels.

Complete Tax Calculation Example: $140,000 Income

Let’s walk through a detailed calculation for someone earning $140,000 in taxable income for 2026:

Step-by-Step Breakdown

Step 1: Apply the Basic Personal Amount

- First $16,452: $0 tax (covered by BPA)

Step 2: Calculate Tax on Each Bracket

- Next $42,071 (14% bracket): $5,889.94

- Next $58,522 (20.5% bracket): $11,997.01

- Remaining $22,955 (26% bracket): $5,968.30

Total Federal Tax Owed: $23,855.25

Effective Federal Tax Rate: 17.04%

Note: This excludes provincial taxes, additional credits (like pension contributions, childcare, medical expenses), and deductions (RRSP, union dues, etc.).

2026 vs 2025: Side-by-Side Comparison

Understanding what changed helps you identify where savings will appear.

2025 Federal Tax Brackets

- 14.5% on the first $57,375

- 20.5% on $57,376 to $114,750

- 26% on $114,751 to $177,882

- 29% on $177,883 to $253,414

- 33% above $253,414

2025 Basic Personal Amount

- $16,129 for incomes below $177,882

- $14,538 for incomes above $253,414

Key Changes in 2026

✓ Lower rate (14% vs 14.5%) for full year ✓ Higher bracket thresholds across all levels ✓ Increased BPA ($16,452 vs $16,129) ✓ 2.0% indexation adjustment ✓ Expanded income ranges before hitting higher rates

Federal Tax Liability Table for 2026

Based on 2026 tax brackets and BPA of $16,452 (assumes no other credits or deductions):

| Taxable Income | Federal Tax Owed | Effective Rate |

| $\$20,000$ | $\$503$ | $2.51\%$ |

| $\$30,000$ | $\$1,903$ | $6.34\%$ |

| $\$40,000$ | $\$3,303$ | $8.25\%$ |

| $\$50,000$ | $\$4,703$ | $9.40\%$ |

| $\$58,523$ | $\$5,890$ | $10.06\%$ |

| $\$70,000$ | $\$7,281$ | $10.40\%$ |

| $\$80,000$ | $\$9,386$ | $11.73\%$ |

| $\$90,000$ | $\$11,491$ | $12.77\%$ |

| $\$100,000$ | $\$13,596$ | $13.59\%$ |

| $\$117,045$ | $\$17,001$ | $14.53\%$ |

| $\$125,000$ | $\$19,081$ | $15.26\%$ |

| $\$140,000$ | $\$23,855$ | $17.04\%$ |

| $\$160,000$ | $\$29,025$ | $18.14\%$ |

| $\$181,440$ | $\$35,185$ | $19.40\%$ |

| $\$200,000$ | $\$40,705$ | $20.35\%$ |

| $\$225,000$ | $\$48,955$ | $21.76\%$ |

| $\$250,000$ | $\$57,205$ | $22.88\%$ |

| $\$258,482$ | $\$59,652$ | $23.08\%$ |

| $\$300,000$ | $\$72,452$ | $24.15\%$ |

| $\$400,000$ | $\$105,452$ | $26.36\%$ |

How to Read This Table

- Taxable Income: Your income after all deductions

- Federal Tax Owed: Tax calculated using progressive brackets

- Effective Rate: Actual percentage of total income paid in federal tax

Notice how the effective rate remains significantly lower than the marginal rate for most income levels—this is the benefit of progressive taxation.

Understanding Tax Indexation: Your Inflation Protection

Indexation is the automatic adjustment of tax brackets and credits to account for inflation. Without it, taxpayers would experience “bracket creep”—being pushed into higher tax brackets without any increase in purchasing power.

How 2.0% Indexation Helps You

Higher Thresholds: You can earn more before entering higher tax brackets Increased Credits: The BPA and other credits rise with inflation Stable Real Tax Burden: Your effective tax rate doesn’t increase solely due to inflation Automatic Protection: No action required—CRA applies indexation automatically

Why 2.0% Matters

The 2026 indexation rate of 2.0% is lower than 2025’s 2.7%, reflecting Canada’s moderating inflation rate. While smaller than previous years, this adjustment still provides meaningful protection for all taxpayers.

Strategic Tax Planning for 2026

Understanding your position within the tax bracket structure opens opportunities for significant savings.

1. Maximize RRSP Contributions

Registered Retirement Savings Plan contributions reduce your taxable income, potentially moving you into a lower bracket.

Strategic Contribution Points:

- Reduce income below $117,045 to avoid the 26% bracket

- Reduce income below $181,440 to avoid the 29% bracket

- Reduce income below $258,482 to maximize BPA benefits

Example Benefit: A taxpayer earning $120,000 who contributes $3,000 to their RRSP drops from the 26% bracket to the 20.5% bracket on that income, saving $165 in federal tax alone (plus provincial savings).

2026 RRSP Contribution Limit: 18% of 2025 earned income, up to $32,490

2. Optimize TFSA Strategy

While Tax-Free Savings Accounts don’t reduce taxable income, they offer tax-free investment growth.

2026 TFSA Contribution Limit: $7,000 (unchanged from 2024-2025)

Best Uses for High-Income Earners:

- Tax-free capital gains (avoiding additional income in higher brackets)

- Emergency fund growth without tax implications

- Supplement to RRSP for retirement planning

3. Leverage Charitable Donations

Donation tax credits reduce your final tax bill and become increasingly valuable at higher incomes.

Federal Credit Rates:

- 15% on the first $200 donated

- 29% on amounts over $200 (33% for highest earners)

Strategic Timing: Group donations across years to exceed the $200 threshold more frequently, maximizing the higher credit rate.

4. Time Income and Bonuses Strategically

If you have control over when you receive income:

Consider Deferring Income If:

- You’re near a bracket threshold

- You expect lower income next year

- You want to preserve the full BPA

Consider Accelerating Income If:

- You’re in a temporarily low-income year

- You expect significantly higher income next year

- You’ve maximized current-year deductions

5. Claim All Eligible Credits and Deductions

Beyond the BPA, numerous credits can reduce your tax burden:

- Canada Employment Amount: $1,433 for 2026

- Public Transit Amount: For eligible transit passes

- Home Office Expenses: If working from home

- Medical Expenses: Amounts exceeding 3% of income

- Tuition and Education Credits: For students or carried forward

- Disability Tax Credit: $9,872 for 2026

- Caregiver Credits: For supporting dependents

Impact Analysis by Income Level

Low-Income Canadians (Under $40,000)

Primary Benefits:

- Full BPA application means minimal or no federal tax

- 14% rate maximizes take-home pay on earned income

- Enhanced benefits from refundable credits (GST/HST, CCB)

Example Impact: A single person earning $30,000 pays just $1,903 in federal tax—an effective rate of 6.34%. The 14% rate and increased BPA save approximately $350 annually compared to the old 15% system.

Middle-Income Canadians ($40,000-$120,000)

This group represents the majority of Canadian workers, including teachers, nurses, trades professionals, administrative staff, and early-career professionals.

Primary Benefits:

- Longest duration in lower tax brackets due to indexation

- Full BPA application (for incomes below $181,440)

- Maximum percentage savings from rate reduction

- RRSP contributions highly effective

Example Impact: A middle-income earner at $80,000 pays $9,386 in federal tax (11.73% effective rate). The combined benefit of the 14% rate, indexation, and higher BPA saves approximately $600-800 annually.

High-Income Canadians (Over $180,000)

High earners still benefit from changes, though the percentage impact is smaller.

Primary Benefits:

- Lower rates apply to first $181,440 of income

- Indexation delays entry into 29% and 33% brackets

- Strategic RRSP contributions most valuable

- Partial BPA still available

Planning Priorities:

- Maximize RRSP room ($32,490 limit for 2026)

- Consider income splitting with spouse

- Leverage charitable donations at 29-33% credit rate

- Explore business structure optimization if self-employed

Example Impact: An earner at $300,000 pays $72,452 in federal tax (24.15% effective rate). While the dollar savings from rate changes are larger, the percentage benefit is smaller than for middle-income earners.

Federal vs Provincial Tax Considerations

Federal brackets represent only part of your total tax burden. Each province and territory maintains separate tax systems.

Provincial Tax Structure Overview

Multi-Bracket Systems: Most provinces use progressive brackets similar to federal (Ontario, BC, Manitoba, Nova Scotia, etc.)

Single-Rate Systems: Alberta uses a flat 10% provincial tax on all taxable income

Separate Collection: Quebec administers its own tax collection independent of CRA

Variable Rates: Provincial rates range from 10% (Alberta) to over 20% (highest Quebec bracket)

Combined Federal-Provincial Examples

Alberta (Flat 10%):

- $80,000 income: ~$9,386 federal + ~$6,355 provincial = $15,741 total

Ontario (Progressive):

- $80,000 income: ~$9,386 federal + ~$3,770 provincial = $13,156 total

British Columbia (Progressive):

- $80,000 income: ~$9,386 federal + ~$4,480 provincial = $13,866 total

Quebec (Separate System):

- Unique calculations with different brackets and credits

Planning Implications

Always calculate both federal and provincial taxes together. Strategies that optimize federal taxes may have different impacts provincially.

Example: RRSP contributions save at your marginal rate for both systems. A $5,000 RRSP contribution in the 26% federal bracket + 12% provincial bracket saves $1,900 total.

Common Questions About 2026 Tax Brackets

How do I know which tax bracket I’m in?

Your tax bracket is determined by your taxable income—not your gross salary. Taxable income is calculated after all deductions (RRSP, union dues, childcare, etc.) are subtracted from your total income.

Does my entire income get taxed at my highest rate?

No. Canada uses a progressive system where only the income within each bracket is taxed at that bracket’s rate. Lower portions of your income are always taxed at lower rates.

When should I make RRSP contributions for 2026?

You can make RRSP contributions for the 2026 tax year from January 1, 2026, through March 2, 2027 (the RRSP deadline for the 2026 tax year).

How do federal changes affect my provincial taxes?

Federal bracket changes don’t directly change provincial brackets, but your taxable income (after federal deductions) flows to your provincial return, so strategies that reduce federal taxes often reduce provincial taxes too.

Will I get a refund in 2027 when filing my 2026 taxes?

Refunds depend on whether your employer withheld more tax than you owe. The lower 14% rate may result in slightly smaller refunds if payroll adjustments account for the change, but your total tax paid will be lower.

Key Takeaways for Canadian Taxpayers

What You Need to Remember

✓ 14% Rate is Permanent: The reduced lowest bracket rate applies to all Canadians for the entire 2026 tax year

✓ Higher BPA Means More Tax-Free Income: $16,452 of income is federally tax-free for most Canadians

✓ Indexation Provides Automatic Protection: 2.0% adjustment prevents inflation-driven tax increases

✓ Plan Around Thresholds: Understanding bracket boundaries helps optimize RRSP contributions and income timing

✓ Provincial Taxes Matter: Always consider your total tax picture, not just federal

✓ Early Planning Pays Off: Understanding 2026 brackets now allows for year-long tax optimization

Action Steps for 2026

- Calculate Your Expected Taxable Income: Include salary, investment income, and other sources

- Identify Your Marginal Tax Bracket: Determine which rate applies to your last dollar of income

- Review RRSP Contribution Room: Check your 2025 Notice of Assessment for available contribution space

- Plan Strategic Contributions: Time RRSP and TFSA contributions for maximum benefit

- Track Deductible Expenses: Keep records of medical expenses, charitable donations, and work-related costs

- Adjust Payroll Withholding if Needed: Speak with your employer if you anticipate significant tax changes

- Consider Professional Advice: Complex situations benefit from accountant or tax planner consultation

Frequently Asked Questions

What are the 2026 federal tax brackets in Canada?

The 2026 federal tax brackets are:

- 14% on income up to $58,523

- 20.5% on income from $58,524 to $117,045

- 26% on income from $117,046 to $181,440

- 29% on income from $181,441 to $258,482

- 33% on income over $258,482

These rates apply only to federal taxes; provincial taxes are additional.

What is the Basic Personal Amount for 2026?

The Basic Personal Amount (BPA) for 2026 is $16,452 for individuals earning $181,440 or less. It phases down to $14,829 for those earning $258,482 or more. If you earn less than $16,452, you pay no federal income tax.

How much federal tax will I pay on $100,000 in 2026?

On $100,000 of taxable income in 2026, you’ll pay approximately $13,596 in federal tax (13.59% effective rate) after applying the Basic Personal Amount. This doesn’t include provincial taxes or additional credits and deductions you may qualify for.

What’s the difference between the 2025 and 2026 tax brackets?

The 2026 brackets feature a full-year 14% lowest rate (compared to 14.5% effective rate in 2025), higher income thresholds due to 2.0% indexation, and an increased Basic Personal Amount of $16,452 (up from $16,129 in 2025).

How does the 14% tax rate save me money?

The 14% rate on the first $58,523 of taxable income saves you approximately 1% on that income compared to the previous 15% rate. For someone earning $60,000, this represents roughly $585 in savings annually, plus additional savings from the increased BPA.

Do the 2026 federal tax brackets include provincial taxes?

No. The federal brackets cover only federal income tax. Each province and territory has separate tax brackets and rates that apply in addition to federal taxes. Your total tax burden is the combination of both systems.

Final Thoughts: Making 2026 Work for You

The 2026 federal tax changes—while modest compared to some previous years—deliver meaningful relief to Canadian taxpayers across all income levels. The combination of the full-year 14% rate, 2.0% indexation, and increased Basic Personal Amount creates opportunities for smart financial planning.

Whether you’re a young professional just starting your career, a middle-income family managing household expenses, or a high earner optimizing tax efficiency, understanding these brackets helps you keep more of your hard-earned income.

Start planning now to maximize your 2026 tax position. Review your income projections, calculate your estimated tax liability, optimize your RRSP and TFSA contributions, and consider consulting with a tax professional for personalized strategies.

Remember: Tax planning is a year-round activity, not just a spring scramble. The earlier you start, the more options you have to reduce your tax burden legally and effectively.